Aradel should be trading between N2000-N3000

While the market may be bearish on Aradel the moment, it should trade much higher

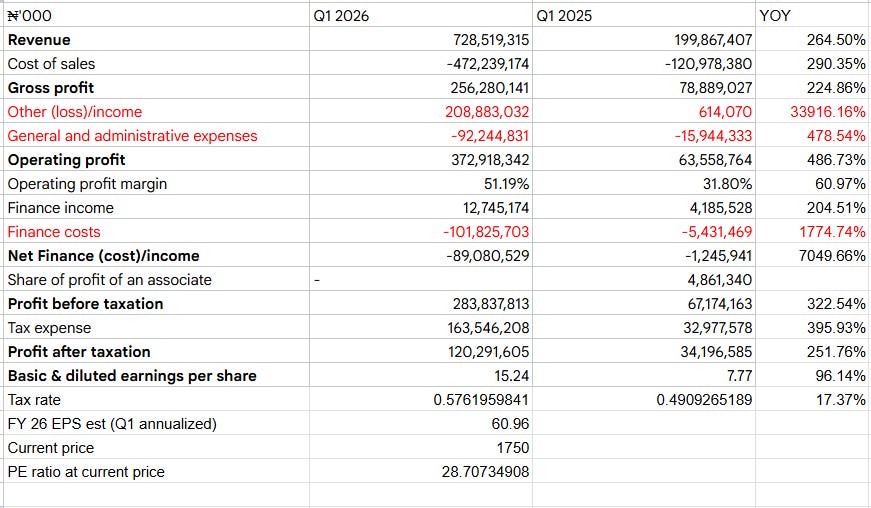

Aradel yesterday dropped its audited Q1 2026 earnings. On surface level, there was a big bounce in revenue and profit after tax. The numbers reflect the additional stake in ND Western acquired by the firm last year.

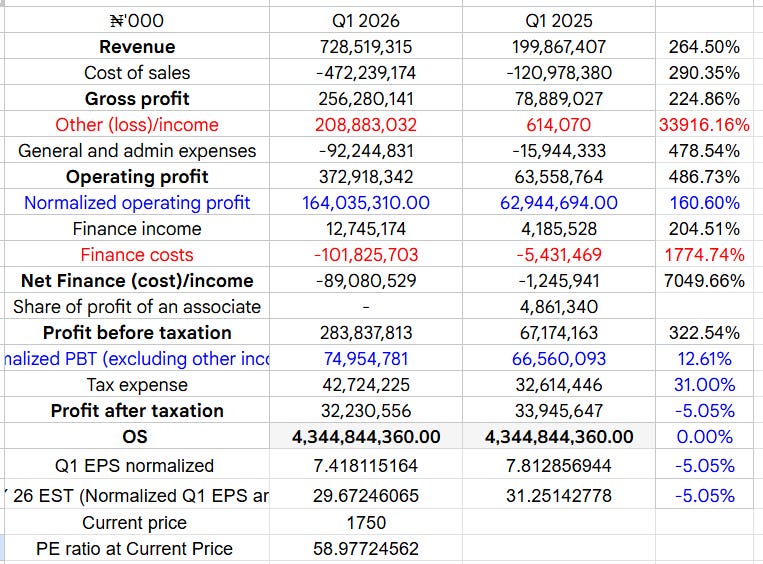

Stripped of other income, and you had a slight dip in profit after tax.

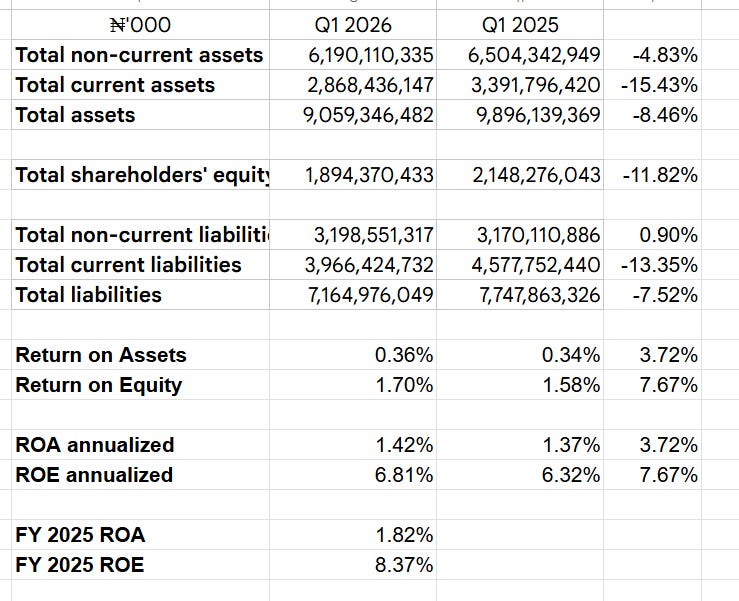

Return on assets and return on equity are a bit weak and may come in lower than last year at the current run rate.

There are a few bright spots in the numbers though. Crude oil profit is up year on year. FY 25 saw a drop in profit after tax.

Annualize the revenue and you have circa N3.1 trillion in revenue for FY 2026. Even though not the most elegant argument, it may have some merit. A firm with N3.1 trillion in revenue should not be trading at a market cap of a N7.6 trillion. It should be trading much higher. How much higher? That’s an individual decision.

A N2,000 to N3,000 thesis

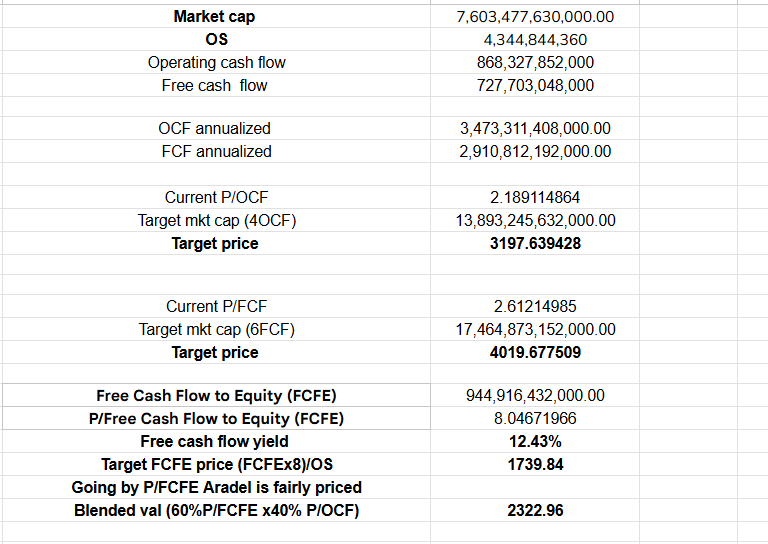

Depending on how you value the stock as shown below. Aradel is either fairly valued or slightly undervalued.

An FCFE target of 8X market cap will have the stock at N1739.84.

Market cap of 4X OCF (operating cash flow) places fair value at N3,197.

Market cap of 6X FCF (free cash flow) places fair value at N4,019.

Blended val (60%P/FCFE x40% P/OCF) gives a fair value of N2,322.96.